Royalty Pool Split Calculator

Divide a royalty pool across writer, publisher, and master sides with participant weights, admin fees, recoupment reserves, source factors, and per-party allocation rows.

Model: Load a named royalty scenario, then adjust the total pool, rights-side percentages, reserve, admin fee, recoupment policy, and participant weights.

Each active participant can receive writer, publisher, and master allocations. Weights are normalized inside each rights side, so the full payable side is assigned even when weights do not total 100.

| Use | Participant | Role | Writer Wt | Publisher Wt | Master Wt | Direct Advance |

|---|---|---|---|---|---|---|

| Participant | Role | Writer Pay | Publisher Pay | Master Pay | Advance Offset | Net Allocation |

|---|---|---|---|---|---|---|

| Calculate to see per-party allocations. | ||||||

| Rights side | Calculator field | Common participants | Allocation note |

|---|---|---|---|

| Writer share | Writer share of pool | Songwriters, composers, lyricists | Weights model the writer-side ownership split |

| Publisher share | Publisher share of pool | Publisher, admin company, writer-owned publisher | Admin fee is deducted before publisher weights pay out |

| Master share | Master share of pool | Artist, label, producer, featured artist | Recoupment can reduce this side before distribution |

| Reserve hold | Recoup reserve | Unmatched claims, returns, dispute reserve | Removed before rights-side percentages are applied |

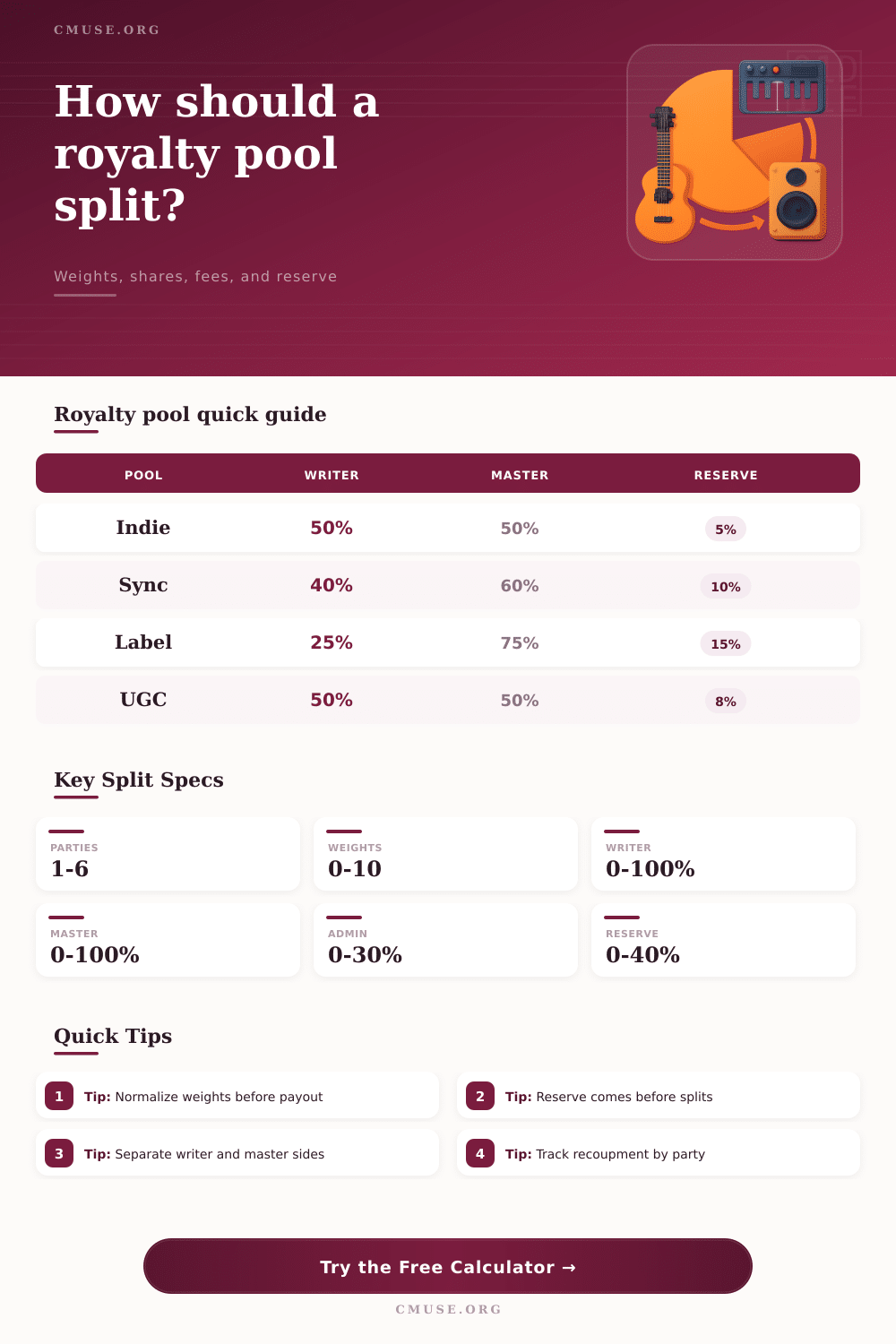

| Preset | Best use | Rights emphasis | Default holdback |

|---|---|---|---|

| Indie Single | Direct release statement | Balanced writer and master sides | Small reserve, light recoupment |

| Sync License Split | One license fee across composition and master | Master-heavy negotiated allocation | Moderate reserve for clearance |

| Writer Camp | Multiple writers with little master ownership | Writer weights drive the split | Low reserve, admin on publisher side |

| Producer Pool | Producer participation in master and writing | Producer receives both writer and master rows | Recoupment may affect master side |

| UGC Micro Pool | Low-certainty platform pool | Blended writer, publisher, and master estimate | Higher reserve for matching issues |

| Policy | Recoup source | Payout effect | Use when |

|---|---|---|---|

| Master side only | Master pool after reserve | Writer and publisher sides still pay | Recording costs recoup only from master royalties |

| Full net pool | Writer, publisher, and master pool | Conservative payout timing | Agreement allows broad cross-recoupment |

| Hold in reserve | Reserve reporting only | No direct deduction from current payout | Balance is tracked but not charged this period |

| Ignore recoupment | No recoupment applied | Payable pool ignores the entered balance | Statement is already post-recoupment |

| Source factor | Multiplier | What it represents | Planning note |

|---|---|---|---|

| Statement pool | 1.00x | Closed accounting amount | Use when total pool is already known |

| Streaming blended pool | 0.85x | Platform pool estimate with normal deductions | Useful for blended DSP statements |

| Sync license pool | 1.20x | Negotiated license value | Good for composition and master license modeling |

| UGC or micro-sync pool | 0.75x | Lower certainty usage matching | Pair with a higher reserve percentage |

| Foreign collection pool | 0.92x | Reciprocal or delayed collections | Use for territory-weighted estimates |

| Entered weights | Calculator behavior | Why it matters | Example |

|---|---|---|---|

| Total equals 100 | Uses entered percentages directly | Clean split sheet behavior | 50, 25, 25 |

| Total above 100 | Normalizes back to 100 | Prevents over-allocation | 60, 60 becomes 50, 50 |

| Total below 100 | Scales active weights up | Assigns the full rights-side pool | 30, 20 becomes 60, 40 |

| Total is zero | Assigns side to first active party | Keeps the calculator from dropping a pool | 0, 0 becomes 100, 0 |

Often the number that is represent on the first line of a royalty statement is not the final amount that the person who own the royalties will recieve. The royalty statement begins with a pool of money that has been earned from various source. A variety of individuals and companies claim the money in that pool.

Thus, it is necessary for individuals to understand the pool of money that is available and how many of those individuals and companies is to receive a share of that pool. Furthermore, the order in which the various deduction are made from that pool has a bearing upon the final amount of royalties that is distributed to those participant. A reserve for returns and unmatched claim is one deduction that is made from the royalty pool prior to determine the percentage of royalties that will go to the writers and publishers that owns the master and publishing rights.

How Royalty Money Is Split

Following establishment of the reserve for returns, an admin fee is applied to the royalty pool, although only to the publisher side of that royalty pool. Following calculation of the admin fees, the company may recoup advances. Recoupment may siphon money from the master side of the royalty pool only, or it may siphon money from the entire royalty pool depending upon the recoupment provision that are established in the licensing and publishing contract.

Thus, the order in which these deduction from the royalty pool are made is important. Next, each of the participants in the royalty pool have a weight associated with their share of the pool. For instance, a producer may have a weight for both the writer and the master side of the royalty pool, while a featured artist may only have a weight for the master side of the royalty pool.

The royalty pool calculator are often programmed with a function that establishes a percentage distribution of the entire royalty pool to each participant in the royalty pool, even if their weight do not mathematically equal 100%. The royalty pool calculator performs this percentage distribution in order to ensure that each participant in the royalty pool is allocated a portion of the pool; otherwise, their weights may not mathematically distribute the royalties to each individual. Furthermore, the weights may mathematically distribute more than 100% of the royalty pool to the participants in the royalty pool; the royalty pool calculation software corrects this overpayment.

Following establishment of each of the participants in the royalty pool, a source factor may be applied to the royalty pool between the royalty statement and the adjusted royalty pool calculation. For instance, streaming rights may have a source factor of 0.85, while sync licenses may have a source factor of 1.20. The source factor is applied to royalty pools prior to any calculation with percentage distributions to ensure that percentage distribution are accurate to the percentage of the royalty pool that is distributed to each participating individual.

After the application of the source factor, determination of the percentage distributions for each participant in the royalty pool, application of the weights of each participant, and application of the admin fee and recoupment calculations, it is possible that the recoupment policy will change the distribution of money within the royalty pool. For instance, some publishing contract will only allow for the master side of the royalty pool to be recouped; other contract may allow for the publisher to recover advances from the entire royalty pool. Furthermore, recoupment policies may only track the balance within the reserve for returns for advances by the master; such a recoupment policy will not touch the balance within the current royalty pool.

Thus, each of these policy will alter the distribution of royalties to each individual within the royalty pool. Therefore, it is important for individuals to understand how each of these policies will impact each of the individuals’ distribution of royalties. Another error that is often made in the calculation of royalties is the error of direct advance.

Each individual that has a royalty statement is often given an advance against the royalties that it is to receive. Thus, an advance is often deducted from the royalty distribution that is calculate for that individual. Such an advance will have an impact upon the distribution of that royalty if it is applied after the initial calculation of the share in the royalty pool; it is possible that the advance will result in a negative royalty distribution to that individual.

Thus, it is important for individuals to understand that this deduction will impact the distribution of royalties to that individual, and that the royalty pool calculation software can calculate both the gross distribution and the net distribution of royalties to that individual after advances are applied. Mistakes are often made in calculating royalties. One of the most common mistake is the error regarding the reserve.

More specifically, some individuals may apply other calculation first before calculating the reserve for returns and advances, which is incorrect. Another of the most common mistakes is entering the weights into the royalty pool distribution software such that the weights do not equal 100% for each of the rights sides; in such cases, the royalty pool calculation software will automatically distribute the share of royalties such that the royalty pool calculation software will make the weights that are entered to each individual. Another of the most common errors is ignoring the admin fee for the publisher; when applied, this will affect the amount that appears to be distribute to the publisher in the royalty pool calculation.

Finally, the most common error that will have the greatest impact upon royalty distributions may be the error of determining the advance for the different types of royalty pools under different recoupment policy. Finally, reference table are often used to show the typical ranges of the different variables of royalty calculations. For instance, indie singles may have reserves and recoupments that differ from those within label master royalty pools.

Sync licenses may have different factor, such as a higher source factor, than other type of royalty pools. Thus, although not rules within the royalty pool calculations, these range help to indicate the typical settings for the variables within royalty pools. The use of these type of royalty calculation scenario analyses will help each of the participants within royalty pool to understand the effects of the different types of royalties.

For instance, determining the effect that changing the reserve percentage will have upon the distribution of royalties to each individual will help each individual within the royalty pool to understand how they can best negotiate their royalties. Additionally, understanding the difference between each type of recoupment policy will help individuals to understand why their royalty distributions may appear to be smaller than those that they had initially calculated. Thus, the goal of establishing these scenario analyses is to allow each individual to understand not just the percentage of royalties that is distributed to each individual, but also to gain an understanding of who is to receive what percentage of royalties.